You Owe How Much?! A No-Nonsense Guide to Getting Out of Debt

Somewhere right now, a person is lying awake at 2 a.m. staring at the ceiling, doing mental math they don't like. Sound familiar? You're not alone. Debt is the most searched personal finance topic in America — and it's not even close. Millions of people every month turn to the internet with some version of the same desperate question: How do I get out of this hole?

Good news: the hole has a ladder. Let's talk about it.

First, Let's Acknowledge the Elephant in the Room

The average American household carries over $100,000 in debt when you factor in mortgages, car loans, student loans, and credit cards. Credit card debt alone now tops $1 trillion nationally. We are, as a country, extraordinarily good at spending money we don't have yet.

How did we get here? Partly culture — we live in a society that treats debt as normal, even sophisticated. "Build your credit!" "Zero percent APR for 18 months!" "You deserve it!" These are the financial equivalent of someone handing you a shovel and saying, "Dig faster." The system is designed to keep you borrowing, because your interest payments are someone else's profit.

The Myth of "Good Debt"

Before we talk solutions, we need to bust a popular myth: the idea that some debt is "good." You've heard this one. Mortgages are good debt. Student loans are an investment. Car loans are just the cost of having a car.

Here's the uncomfortable truth: debt is a tool, and like any tool, it can hurt you if misused. A mortgage on a home you can genuinely afford? Reasonable. A $60,000 student loan for a degree with poor job prospects? Not so much. A $45,000 truck financed over 84 months for someone making $40,000 a year? That's not transportation — that's a financial anchor.

The label "good" or "bad" matters far less than the question: Can you actually afford this, and is it moving you toward financial freedom or away from it?

The Snowball vs. The Avalanche

There are two main strategies for paying off multiple debts, and people argue about them on the internet with a passion usually reserved for sports teams.

The Debt Avalanche is mathematically optimal. You list your debts in order of interest rate — highest to lowest — and attack the most expensive debt first while making minimum payments on everything else. Over time, you pay less total interest. It's efficient. It's logical. It's what a spreadsheet would recommend.

The Debt Snowball ignores the math and wins anyway. You list your debts smallest to largest by balance and pay them off in that order. You get quick wins. A $400 medical bill disappears in a month. Then a $900 store card. Then a $2,200 personal loan. Each payoff is a dopamine hit, a proof of concept, a reason to keep going.

Research consistently shows that the snowball method results in more people actually finishing their debt payoff journey, precisely because it accounts for human psychology. Motivation is a resource. The snowball method replenishes it. Pick the approach that keeps you in the game.

The Budget Is Not the Enemy

Many people avoid making a budget for the same reason they avoid stepping on a scale: they're afraid of what they'll find out. But a budget isn't a punishment — it's a map. You cannot navigate out of debt without one.

A budget doesn't have to be complicated. At its most basic, it's just answering two questions every month: What money is coming in? and What money is going out? When those two numbers don't match up the way you'd like, the budget tells you where to make changes before your bank account does.

Write down every income source and every expense — rent, utilities, groceries, subscriptions, that coffee you buy four times a week (yes, that one too). Most people are genuinely surprised by what they find. The budget makes the invisible visible, and you can't fix what you can't see.

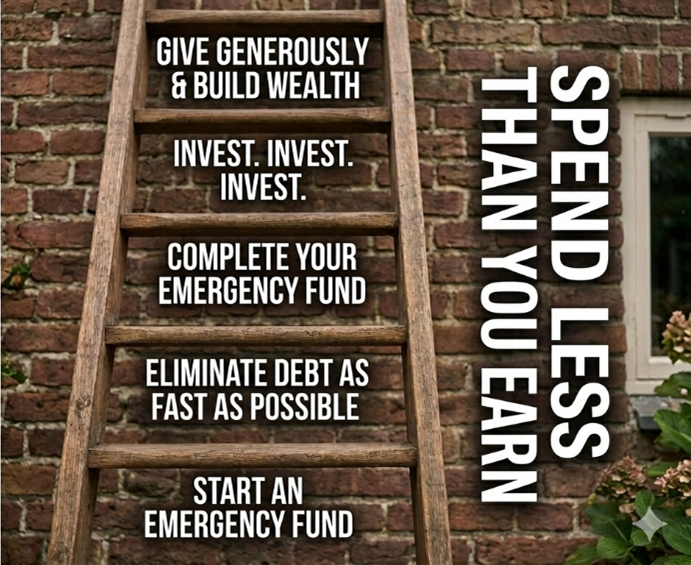

The Radical Power of the Emergency Fund

Here is a pattern that traps millions of people in debt permanently: they work hard, pay down a credit card, and then the car breaks down. Back to square one.

An emergency fund breaks this cycle. Even a small one — $1,000 set aside in a savings account you don't touch — acts as a buffer between you and the next unexpected expense. It's not an investment. It's not supposed to grow. It's insurance against the chaos of real life, and it is the single most important first step before aggressively paying down debt.

Once your debt is gone, the goal expands: build that emergency fund up to three to six months of living expenses. This is the financial equivalent of a seatbelt. You hope you never need it. You are very glad to have it when you do.

The Boring Truth About Getting Wealthy

Here's the part nobody wants to hear: there is no secret. There is no app, no side hustle, no investment strategy that replaces the fundamentals. The path out of debt — and eventually toward real financial security — is the same one it's always been.

Spend less than you earn. Eliminate debt as fast as possible. Build savings. Invest consistently over time. Repeat for decades.

This advice is profoundly not shocking. It doesn't go viral. Nobody's making a documentary about it. But the families who follow it — quietly, consistently, without fanfare — end up with options. They can quit jobs they hate. They can help their kids. They can retire without panic. They sleep well at night.

That person lying awake doing ceiling math at 2 a.m.? They don't have to do that forever. The ladder is right there.